By Tom O’Leary

Japan remains an important economy, the third largest in the world behind China and the US. If the EU Single Market is considered as a single economy it is the fourth largest in the world, although considerably smaller than each of these.

But it is a much less important economy than it used to be. A period of extraordinary growth in real GDP in the post-War period gave way to recession and then virtually complete stagnation from 1990 onwards. From 1950 to 1990 the Japanese economy increased by over 13 times, much faster than the world economy (Angus Maddison data). But in the 28 years since the Japanese economy has expanded by less than a third (OECD data).

In 1990 Japan accounted for 8.6% of world GDP (Maddison). By 2018 this had fallen to 4% of world GDP (World Bank). This period of economic stagnation was first known as ‘Japan’s lost decade’. But it has dragged on to become the ‘lost generation’.

This period bears closer scrutiny, being the most recent period when an advanced industrialised country stagnated over such a prolonged period, not least because the G7 economies as a whole have been effectively stagnating since the crash of 2008.

The myth of Japanese investment

One of the abiding myths about the period of the Japanese crisis from 1990 onwards is that the government tried to revive the economy with a sharp increase in public works spending. It is further frequently asserted that the governments were so useless that it mainly built ‘bridges to nowhere’ and that they eventually ran out of money. It is also asserted that China’s public works investment will go the same way, and that no government in the West should be so foolish to emulate it now, and that the Corbyn/McDonnell investment programme is therefore bound to fail too.

This Thatcherite morality tale is very widely repeated. But it is completely untrue.

What is true is that the Japanese governments frequently announced large new public works spending, often with great fanfare. But it is not true that they increased public sector investment.

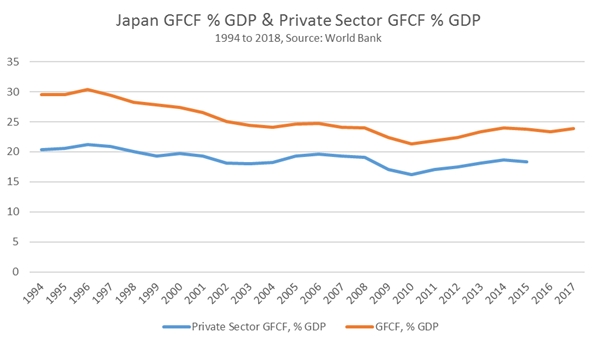

Chart 1. below shows both Japanese total Gross Fixed Capital Formation (GFCF) as a percentage of GDP, as well as the private sector’s GFCF as a percentage of GDP. There is a clear downtrend trend in total Investment, or GFCF.

Chart 1.

The decline in the contribution of Investment to GDP is exactly as would be expected in a period of outright stagnation, given the decisive contribution of Investment to GDP growth. In 1990 (not shown in the chart) total Japanese GFCF amounted to just over 34% of GDP. This was not massively below the post-World War II peak of 38.7% in 1973. But by 2010 total GFCF had fallen to just 21.3% of GDP. From accounting for just over a third of Japanese GDP, GFCF slipped to little more one-fifth of GDP and has not recovered fully since that time.

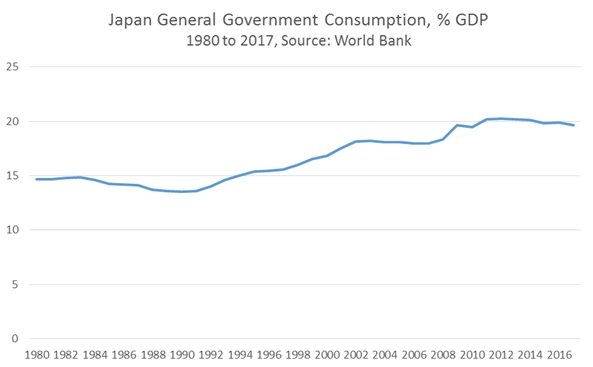

To be clear, this is quite separate from the Consumption of the Japanese public sector which did rise sharply in response to the crisis. This is shown in Chart 2. Below. Government Consumption rose throughout most of the crisis period, at least until 2010. But increased Consumption cannot sustainably lift production because it provides no new means of production. That requires Investment to create new productive capacity. Put another way, attempting to use Consumption to drive GDP higher over a sustained period will end in failure on both counts.

Chart 2. Japanese Government Consumption, % GDP

Returning to Chart 1 once more, it should be noted that the decline in Investment was not driven solely by the private sector. In 1994 (the earliest available date for the disaggregated private sector data), private sector GFCF accounted for 20.4% of GDP. By 2015 (latest available data) this had slipped to 18.3% of GDP.

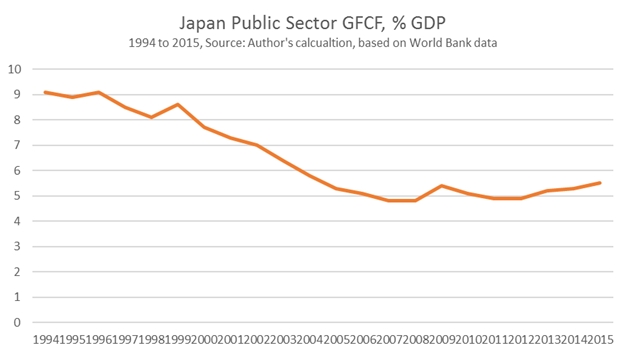

This is highlighted in Chart 3. below. This shows the calculated level of general government GFCF as a percentage of GDP, arrived at by subtracting private sector GDP from the total GFCF.

Chart 3. Japan General Government GFCF as % of GDP

Over the period general government GFCF as a percentage of GDP fell from 9.1% in both 1994 and 1996 to a low-point of 4.8% of GDP in 2007 and 2008. It has only recovered to 5.5% in 2015. Therefore the total loss in terms of public sector Investment has been 3.6% of GDP, while the total cumulative loss in private sector Investment has been 2% of GDP over the same period.

Far from Japanese government assertions, echoed by a wide array of analysts and pundits, that public Investment was increased but it proved useless in reviving the economy, the opposite is the case. The Japanese public sector slashed its own Investment, almost cutting it in half. The cut in public sector Investment was mainly responsible for the decline in total Investment.

This cut in public Investment was much greater than the simultaneous cut in private sector Investment – despite being a much smaller initial value. Throughout the process, it was the fall in public sector Investment which also led the way, and private sector Investment did not reach its own low-point until three years after the public sector (spurred on by the fall in the level of profits in 1992, which have never properly recovered).

A public investment diversion

As noted above, the change in Japanese public Investment was a fall of 4.3% of GDP from its 1994 (and 1996) level to its low-point in 2007. Even the most strongly growing economies would struggle if any factor was reduced by 4% of GDP. But the decisive role of Investment in accounting for GDP growth means that slump and stagnation was effectively unavoidable.

What caused the Japanese public sector to choke off Investment, slow the economy to stagnation and lead the Japanese private sector into cutting its own Investment? According to US Treasury data (pdf) Asian holdings of US Treasuries (government bonds) rose from $84 billion in 1984 to $283 billion in 1989 and upwards to $418 billion in 1994. As the US Treasury notes, these are overwhelmingly held by Japan.

Low levels of Asian (mainly Japanese) US Treasuries’ holdings in 1984 ballooned fivefold in just 10 years. In relation to Japanese GDP, total Asian holdings were less than 1% in 1984 and approximately 10% in 1994, even taking into account the surge in the value of the Yen over the same period.

That surge in the Yen did not occur simply as a result of market mechanisms. In 1985 the Reagan Administration, struggling with the accumulated debt of the Viet Nam war and recession of the early 1980s, insisted that other countries, Japan, West Germany, France and Britain sell US Dollars to engineer a depreciation which would make US industry more competitive. The US allies were also obliged to cut their own Investment and increase Consumption, partly to boost US exports. This agreement was formalised in the Plaza Accord of 1985. It also allowed the US to maintain very large budget deficits as it pursued the Cold War arms race to destruction.

The effect on Japan and Japanese industry was profound and dramatic. In February 1985 there were 260 Japanese Yen to the US Dollar but by 1987 the exchange rate had fallen to 121. This was excruciating for Japanese industry, which now struggled to compete internationally because of this more-than-doubling in the exchange rate value of the Yen.

The Japanese government in particular was obliged to sharply increase its purchases of US Treasuries, under threat of hollowing out Japanese industry via the exchange rate. This demand was later reinforced under the separate Louvre Accord. The author of the policy was the US administration under Reagan.

The widely-repeated claim that Japanese public Investment failed to rescue the Japanese economy is no more true for repetition. The opposite is the case. The cut to public Investment was decisive in causing the slump, being both earlier and deeper than the cut in private Investment. Instead, the Japanese government followed US demands to ‘stimulate demand’, that is increase Consumption in its own economy.

Both of these policies, the cut in Japan’s public Investment and the increase in public Consumption were the effects of the US measures to support its own economy, fund its budget deficit and hugely increase its military spending. But it has hobbled the Japanese economy for almost three decades now.

Currently, but for different reasons the US is once more looking to overseas sources of capital to maintain current US living standards and increase spending. How it is attempting to engineer that inflow this time around will be examined in a follow-up piece.

Recent Comments