By Tom O’Leary

The claim from the Tory government and its army of media supporters that the latest Budget has ended austerity is completely false. It is very important for the left and the labour movement as a whole that they grasp the character of the new attacks to come, so that they can resist them.

In effect, this is a Tory government of a new type. Previously, since austerity was first implemented in 2010, the Tory governments have transferred incomes from workers and the poor to big business and the rich. This is in the hope that both increased rates of exploitation and the transfers of funds themselves will encourage business investment. But the encouragement to private investment has been a dismal failure. Private investment growth is officially forecast to be zero this year.

The new Tories want to provide further inducements to private sector investment by increasing public sector investment. SEB has argued vociferously for increased public investment over a prolonged period. This not investment for its own sake, but to increase the productive capacity of the economy (adding to the means of production) as the most decisive factor in raising the output of the economy and therefore prosperity.

But these Tories intend the opposite. They want to increase the rate of exploitation further, provide incentives to private business to investment, and intend to do this by funding with investment with yet another reduction of public services and (probably) public sector pay. They will further shift the burden of the crisis onto the shoulders of workers and the poor.

Summary

The key points of this piece can be summarised below. Readers who need a fuller explanation and data can read the article in full. All data is taken either from the Office of Budget Responsibility (OBR) Economic and Fiscal Outlook or the Treasury Red Book, unless specified.

The key points are as follows:

- Government current spending is being cut over the medium-term.

- There is a one-off boost, to cope with the effects of their own disastrous Brexit

- The projected rise in government investment (if it materialises) will still leave total government expenditure lower than in recent years

- This means that the rise in public investment is more than being funded by further attacks on public services and public sector workers

- There is a significant projected increase in net government borrowing. This is despite a fall in debt interest payments, which themselves are being used to boost spending in the short-term

- This is not ‘deficit-financed growth’, as has been claimed. It is the effect of weaker growth on public finances, pushing both tax revenues lower and automatic outlays (such as welfare payments) higher

- In fact, the current year for which the OBR provides an estimate and the subsequent 5 years’ forecasts are the weakest on record for such a prolonged period

- Taken together, SEB can find no recorded 10-year period of real GDP growth where every year is below 2%. This is what the actual recent growth years’ growth rates will amount to, combined with the OBR forecasts

- There is a sharp one-off rise in government current spending next year. This is not to combat the effects of the coronavirus crisis, which is current. Instead, it follows the withdrawal from the EU at the end of this year. It clearly indicates the government expects a very negative outcome from the Brexit it is planning

- There is nothing substantial in the Budget to address the climate crisis, and the need for large-scale investment in renewable energy production, or conservation

Austerity resumed

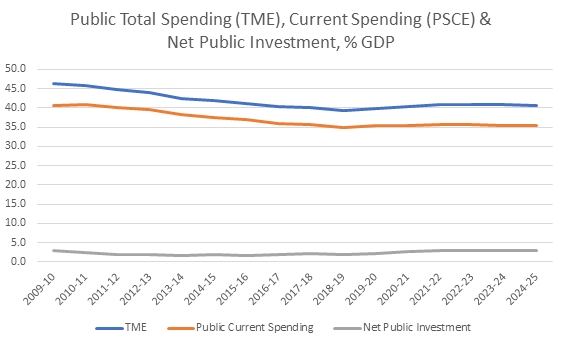

Despite the mass of commentary suggesting that austerity is over, it is very simple to demonstrate that is not the case. The chart below is taken from the OBR databank and shows total for public spending (TME), current (or day-to-day spending, PCE) and net public spending as a percentage of GDP.

Chart 1. UK Public Spending Totals, Current Spending and New Public Investment, as a % of GDP

The chart lines show a downward trend of total government spending. For the 6 years of OBR estimates and forecasts from 2019/20 to 2024/25 average TME (total government spending) is 40.5% of GDP. For the preceding 6 years it was 40.8%. Total government spending will be lower and austerity is not ending at all.

The big impact will be felt by public current spending. Over the same 6-year periods, Public Sector Current Spending (which includes health, education, welfare and so on) will fall to 35.5% of GDP, from 36.5% of GDP.

By contrast public sector net investment is projected to rise from 2% of GDP last year to 3% by the end of the 6 years of the OBR’s forecast period. But it should be clear, it is ordinary people who most rely on public services who will be paying for this increase. Furthermore, as the OBR itself points out, there is a persistent and large shortfall between the projections for public sector investment and what actually takes place. Planning investment is not the same as delivering it.

A significant one-off boost to spending

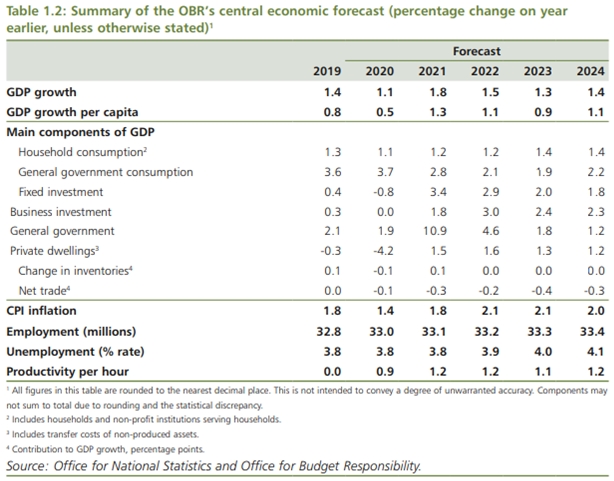

The basis for all the hyperbole and false claims about the Budget is because of a one-off increase in government spending next year. This can be shown in one of the key tables from the Treasury’s Red Book.

As the table shows general government spending receives a very large boost in 2021, rising by 10.9%. This falls back in the following year and austerity returns in 2023 and 2024. It is important to note that the growth rate of this measure of government spending is even slower than in the most recent years, 1.8% and 1.2% in 2023 and 2024, compared to 2.1% and 1.9% in 2019 and 2020.

This increase in government spending is not coronavirus-related, which is a current crisis that the government will be hoping is over before the end of this year. Instead, it is a response to the Withdrawal Agreement from the EU which does end in December of this year. Clearly, the government expects a large negative shock from the Brexit it intends to carry out, and the increased spending is an attempt to offset its worst effects.

The attempt is only partly successful, using their own data. Real GDP growth is expected to rise to 1.8% in 2021. However, general government expenditure accounts for about 40% of GDP, so a one-off increase of nearly 11% should lead directly to a boost in GDP of well over 4%. But the projected increase is just a fraction of that, with real GDP rising from just 1.1% in 2020 to a very modest 1.8% in 2021, when the spending is to take place. Clearly, the implicit assumption is that without the one-off spending splurge, growth would be sharply negative with the planned Tory Brexit.

Miserably low growth

The official projections for real GDP growth are a terrible indictment of government economic failures. This includes but is not confined to their own assessment of the further damage they will inflict with their preferred Brexit outcome. As the Treasury’s Table 1.2 above shows, there is no single year in which real GDP growth reaches 2% in the recent data and the forecast period.

This is unprecedented. It would amount to at least a 9-year period of real growth below 2%, a lost decade. There is no equivalent in the modern era of such sluggish growth, in either the Great Depression or the Long Depression at the end of the 19th century.

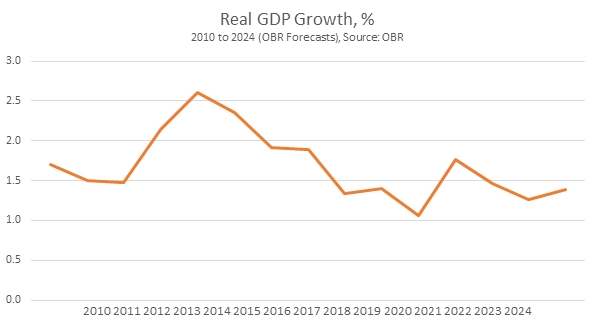

In fact, as Chart 2 below shows, the official outlook for growth is even worse in coming years than the period immediately behind us, in the years following the Great Recession in 2008.

Chart. 2 Real GDP Growth, 2010 to 2024 (Forecast)

This unprecedentedly weak growth has a series of wide-ranging effects, depressing any rise in living standards or improvement in public services. It also has the consequence of damaging public finances, lowering the growth in government taxation revenues and automatically pushing some government spending higher, for example in some welfare payments. This is the cause of the large deficits in public finances that are forecast.

This is not ‘deficit-financed growth’ as has been claimed; there is no growth and the economy slows. And, as already noted total government spending will fall. These deficits are a reflection of economic weakness, not ‘keynesian pump-priming’.

The multiple crises

There are a series of crises that the government is failing to address: coronavirus, the weakness of the economy, the damage from its own intention to crash out of the EU without a deal, the crisis in public services, the unprecedented weakness in the economy and the existential threat of catastrophic climate change. Measured against any of these challenges the government’s response has been woeful.

On the coronavirus crisis, at every turn, it has unpicked the measures praised by the World Health Organisation and enacted in China and Viet Nam. Every excuse is made for inaction, that masks are not perfect, testing is not 100% accurate, there is no point in heat-testing or even hand gels at the airports, and so on. Instead, it has relied on measures to correct some of the economic effects of coronavirus spreading. These steps, and many more will need to be taken. But they are pointless unless and until government is bearing down on the spread on the virus itself, which is clearly not the case.

This will put enormous strain on the economy and public services, especially the NHS (but also care for the elderly and education, among others). Public services are already buckling under impact of a decade of austerity. The UK already has below-average ratio of nurses to the population, 7.9 per thousand compared to 9.0 for the OECD as a whole. The only comparably high-income country with a lower nurse/population is Italy (OECD data).

It is clear that the increased spending in 2021 is not coronavirus-related. Instead, it is a response to the effects of its own determination to pursue a hugely damaging No Deal Brexit, presumably in order to do a deal with Trump and adopt US business and labour market norms. The government’s own forecasts show that a huge increase in spending to offset its Brexit will produce barely a flicker of growth.

The planned increase in public investment is long overdue. But it is very unlikely to produce either the transformation of ‘levelling-up’ across the country or the necessary corrective to abysmally low productivity growth. For accuracy, the OBR forecasters do not expect either outcome.

One neglected factor, well established in classical economics from Smith onwards, is that the effectiveness of all investment is determined by the scope of the market. Any Brexit that takes this economy outside the customs union will necessarily reduce the effectiveness of all investment, because the market will also be severely contracted.

Finally, despite hosting COP26 in Glasgow later this year, it is clear that the Budget contains no plan to address the climate crisis with decisive action. Instead, this a government that has tried to press ahead with plans such as the third runway at Heathrow and a road-building programme regardless of the law. There was not even a pale imitation of Labour’s Green New Deal, or anything similar. The Green New Deal is precisely the required, targeted and ‘shovel-ready’ programme that could be implemented with large-scale state investment – and is absolutely necessary. Instead, it seems likely that The Tory recipe will be to search for new business-friendly projects, such as more roads, and local and haphazard local projects.

When this fails to transform the economy, no doubt there will be a new ideological offensive against public investment of all types. But by then, US companies may be in control of large swathes of the public services in this country.

Recent Comments